Price Determination

Price is not the only factor in making purchasing decisions. However, all other things being equal, it is the most important. In the average manufacturing company, purchases account for about 50% of the cost of goods sold, and any savings made in purchase cost has a direct influence on profits.

However, remember that “you only get what you pay for.” The trick is to know what you want and not pay more than necessary. When a purchase is made, the buyer receives a package of function, quantity, service, and price characteristics that are suited to the individual’s needs. The idea of “best buy” is the mixture that serves the purpose best.

Basis for Pricing

The term “fair price” is sometimes used to describe what should be paid for an item. But what is a fair price? One answer is that it is the lowest price at which the item can be bought. However, there are other considerations, especially for repeat purchases where the buyer and seller want to establish a good working relationship. One definition of a fair price is one that is competitive, gives the seller a profit, and allows the buyer ultimately to sell at a profit. Sellers who charge too little to cover their costs will not stay in business. To survive, they may attempt to cut costs by reducing quality and service. In the end, both the buyer and seller must be satisfied.

Since we want to pay a fair price and no more, it is good to develop some basis for establishing what is a fair price.

Prices have an upper and a lower limit. The market decides the upper limit. What buyers are willing to pay is based on their perception of demand, supply, and their needs. The seller sets the lower limit. It is determined by the costs of manufacturing and selling the product and profit expectation. If buyers are to arrive at a fair price, they must develop an understanding of market demand and supply, competitive prices, and the methods of arriving at a cost.

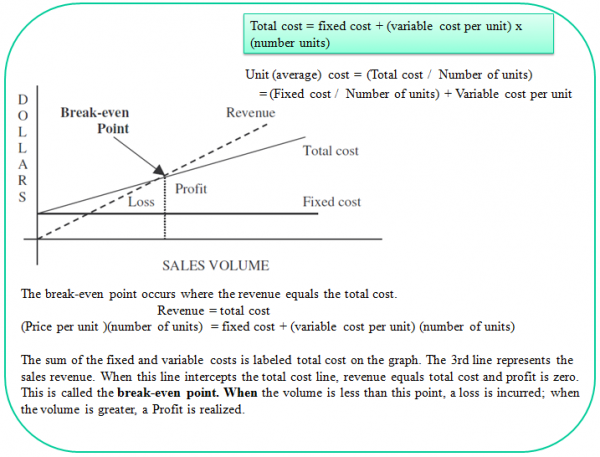

One widely used method of analyzing costs is to break them down into fixed and variable costs. Fixed costs are costs incurred no matter the volume of sales. Examples are equipment depreciation, taxes, insurance, and administrative overhead. Variable costs are those directly associated with the amount produced or sold. Examples are direct labor, direct material, and commissions of the sales force.

Example To make a particular component requires an overhead (fixed) cost of $5000 and a variable unit cost of $6.50 per unit. What is the total cost and the average cost of producing a lot of 1000? If the selling price is $15 per unit, what is the break-even point?

Answer :

Total cost = $5000 + ($6.50 x $1000) = $11,500

Average cost = $11,500 ± 1000 = $11.50 per unit

Break-even point: Let X = number of units sold

$15X= $5000+ $6.5X

$8.50X = $5000

X = 588.2 units

Break-even occurs when 588.2 units are made and sold.

Price Negotiation

Prices can be negotiated if the buyer has the knowledge and the clout to do so. A small retailer probably has little of the latter, but a large buyer may have much. Through negotiation, the buyer and seller try to resolve conditions of purchase to the mutual benefit of both parties. Skill and careful planning are required for the negotiation to be successful. It also takes a great deal of time and effort, so the potential profit must justify the expense.

One important factor in the approach to negotiation is the type of product. There are four categories:

1. Commodities. Commodities are materials such as copper, coal, wheat, meat, and metals. Price is set by market supply and demand and can fluctuate widely. Negotiation is concerned with contracts for future prices.

2. Standard products. These items are provided by many suppliers. Since the items are standard and the choice of suppliers large, prices are determined on the basis of listed catalog prices. There is not much room for negotiation except for large purchases.

3. Items of small value. These are items such as maintenance or cleaning supplies and represent purchases of such small value that price negotiation is of little purpose. The prime objective should be to keep the cost of ordering low. Firms will negotiate a contract with a supplier that can supply many items and set up a simple ordering system that reduces the cost of ordering.

4. Made-to-order items. This category includes items made to specification or on which quotations from several sources are received. These can generally be negotiated.