8. Purchasing

Purchasing refers to a business or organization attempting for acquiring goods or services to accomplish the goals of the enterprise. Though there are several organizations that attempt to set standards in the purchasing process, processes can vary greatly between organizations. Typically the word “purchasing” is not used interchangeably with the word “procurement”, since procurement typically includes Expediting, Supplier Quality, and Traffic and Logistics (T&L) in addition to Purchasing.

Purchasing managers/directors, and procurement managers/directors guide the organization’s acquisition procedures and standards. Most organizations use a three-way check as the foundation of their purchasing programs. This involves three departments in the organization completing separate parts of the acquisition process. The three departments do not all report to the same senior manager to prevent unethical practices and lend credibility to the process. These departments can be purchasing, receiving; and accounts payable or engineering, purchasing and accounts payable; or a plant manager, purchasing and accounts payable. Combinations can vary significantly, but a purchasing department and accounts payable are usually two of the three departments involved.

When the receiving department is not involved, it's typically called a two-way check or two-way purchase order. In this situation, the purchasing department issues the purchase order receipt not required. When an invoice arrives against the order, the accounts payable department will then go directly to the requestor of the purchase order to verify that the goods or services were received. This is typically what is done for goods and services that will bypass the receiving department. A few examples are software delivered electronically, NRE work (non reoccurring engineering services), consulting hours, etc.

In oracle EBS another ferature is avaiable which four way matching which invoices purchasing, Receving, Quality/Inventory and payable departments.

Choosing the right material requires input from the marketing, engineering, manufacturing, and purchasing departments. Quantities and delivery of finished goods are established by the needs of the marketplace. However, manufacturing plan-fling and control (MPC) must decide when to order which raw materials so that marketplace demands can be satisfied. Purchasing is then responsible for placing the orders and for ensuring that the goods arrive on time.

The purchasing department has the major responsibility for locating suitable sources of supply and for negotiating prices. Input from other departments is required in finding and evaluating sources of supply and to help the purchasing department in price negotiation. Purchasing. in its broad sense, is everyone’s business.

Purchasing : Impact on Cost & Profit

Historically, the purchasing department issued purchase orders for supplies, services, equipment, and raw materials. Then, in an effort to decrease the administrative costs associated with the repetitive ordering of basic consumable items, "blanket" or "master" agreements were put into place. These types of agreements typically have a longer duration and increased scope to maximize the quantities of scale concept. When additional supplies were required, a simple release would be issued to the supplier to provide the goods or services.

Another method of decreasing administrative costs associated with repetitive contracts for common material, is the use of company credit cards, also known as "Purchasing Cards" or simply "P-Cards". P-card programs vary, but all of them have internal checks and audits to ensure appropriate use. Purchasing managers realized once contracts for the low dollar value consumables are in place, procurement can take a smaller role in the operation and use of the contracts. There is still oversight in the forms of audits and monthly statement reviews, but most of their time is now available to negotiate major purchases and setting up of other long term contracts. These contracts are typically renewable annually.

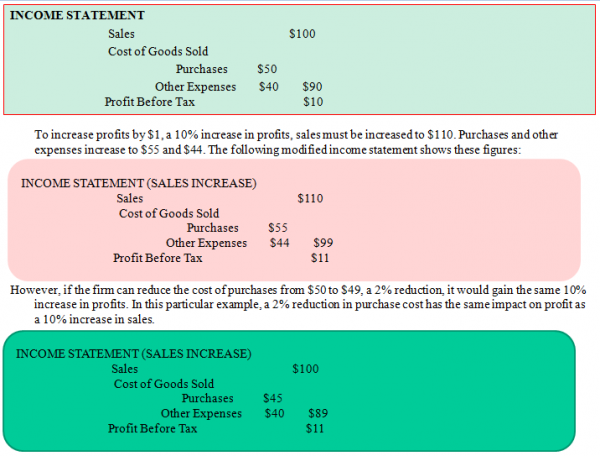

On the average, manufacturing firms spend about 50% of their sales dollar in the purchase of raw materials, components, and supplies. This gives the purchasing function tremendous potential to increase profits. As a simple example, suppose a firm spends 50% of its revenue on purchased goods and shows a net profit before taxes of 10%. For every $100 of sales, they receive $10 of profit and spend $50 on purchases. Other expenses are $40. For the moment, assume that all costs vary with sales. These figures are shown in the following as a simplified income statement:

Purchasing objectives

Missed deliveries can create havoc for manufacturing and sales, but purchasing can reduce problems for both areas, further adding to profit. The objectives of purchasing can be divided into 4 categories:

- Obtaining goods and services of the required quantity and quality,

- Obtaining goods and services at the lowest cost,

- Ensuring the best possible service and prompt delivery by the supplier,

- Developing and maintaining good supplier relations and developing potential suppliers.

To satisfy these objectives, some basic functions must be performed:

- Determining purchasing specifications: right quality, right quantity and right delivery (time and place);

- Selecting supplier (right source);

- Negotiating terms and conditions of purchase (right price);

- Issuing and administration of purchase orders.